Revolving vs Installment Credit — Why You Probably Need Both, and How to Know What You Can Actually Afford

By How Much+ Editorial Team · Published 2026-06-05 · Last updated: 2026-06-05 · 10 min read

A plain-English breakdown of how revolving credit and installment credit each affect your score, your loan approvals, and your real borrowing power — plus how to use your actual leftover income to know what you can afford.

Parts of this article were drafted with AI assistance and reviewed by a human editor. This is general educational content, not personalized advice.

By the How Much+ Editorial Team · Published June 5, 2026

A short note: this article was drafted using AI as a writing assistant and reviewed by a human editor. The information is general — it's not personalized financial or legal advice.

Most people learn how credit works the hard way — after they've already been told no on something they really needed. The first car loan. The first apartment. The first time a credit card company quietly cuts their limit and the math stops working.

The thing nobody tells you in a single clear sentence is this: there are two completely different kinds of credit, they work in different ways, and most lenders want to see you've used both before they'll trust you with the bigger stuff. If you only have one kind, your credit score will hit a ceiling. If you misuse either kind, the damage shows up in different ways.

This is the short, real-world version of how revolving credit and installment credit work, why both matter, and how to use what's left over after you cover your real expenses to make a smart call on what you can actually afford to borrow.

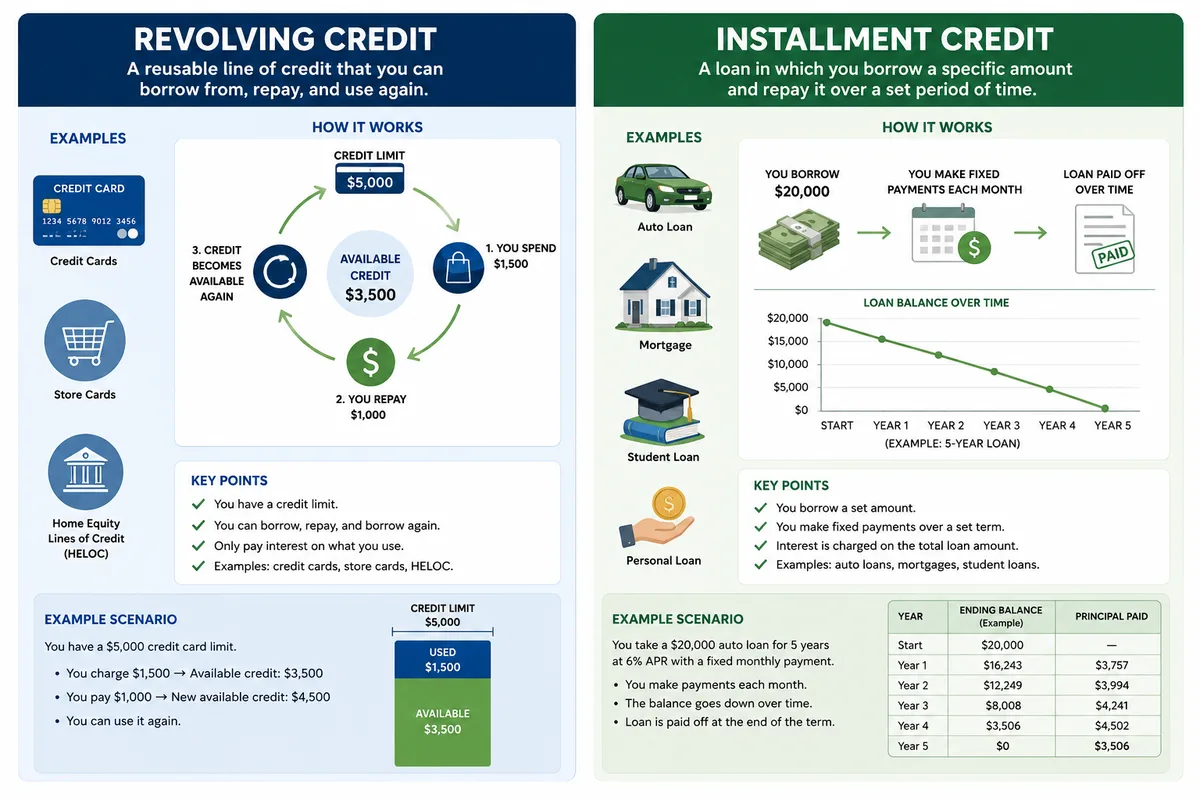

The two kinds of credit

Revolving credit is the kind that opens and closes. Credit cards. Lines of credit. Home equity lines of credit (HELOCs). You're given a maximum amount you can borrow. You borrow some of it, pay it back, borrow it again. As long as you stay under the limit and make your minimum payments, the account keeps working. There's no end date.

Installment credit is the kind that ends. Auto loans. Mortgages. Student loans. Personal loans. You borrow a fixed amount up front. You pay it back in fixed monthly payments over a set period — 36 months, 60 months, 30 years. When you've made the last payment, the loan is closed.

That's the whole difference at the surface. But underneath, the way these two kinds of credit affect your score and your future borrowing power is very different. Knowing which is which — and how each one is judged — is how you stop being surprised by a lender's decision.

How each one weighs on your credit score

Your FICO credit score is built from five factors. The two biggest are payment history (about 35%) and amounts owed (about 30%). Then comes length of credit history (about 15%), new credit (about 10%), and credit mix (about 10%).

Of those five factors, credit utilization sits inside "amounts owed" and is one of the most powerful single levers in your score. And credit utilization only applies to revolving credit — it's the percentage of your available credit you're currently using.

If you have a credit card with a $1,000 limit and a $500 balance, your utilization on that card is 50%. The general rule lenders prefer is keeping it under 30%, and the top-end credit scores usually come from people keeping it under 10%. This is why someone with a great income can have a mediocre score — they're using too much of their available revolving credit at the moment the score is checked.

Installment loans don't have utilization in the same way. A car loan that's 80% paid off doesn't hurt your score the way a credit card that's 80% maxed does. In fact, paying down an installment loan over time consistently builds your payment history — the biggest factor of all — without the utilization penalty hanging over your head.

Then there's the credit mix factor. About 10% of your score comes from showing that you can handle different types of credit responsibly. Someone who only has credit cards is missing this piece. Someone who only has a single auto loan is missing it too. The boost from having both — and paying both on time — is small but real, and it's often the difference between a 750 score and an 800.

Getting one type of credit does NOT guarantee you can handle the other

This is the most important and most-missed point. The two types of credit teach you different financial habits, and being good at one doesn't mean you're good at the other.

Revolving credit teaches you discipline around temptation. The line of credit is always there. The card is in your wallet. The harder skill is choosing not to use it when you don't need to. People who fail at revolving credit usually fail because they treat the limit as money they have, not money they could borrow.

Installment credit teaches you discipline around commitment. Once you sign, you owe the same payment every month for years. You can't reduce it because you had a slow week. The harder skill is being honest with yourself about whether the payment fits your real income, including the months that come in light.

Both kinds of credit punish the same underlying mistake — borrowing more than your income can support — but they punish it on different timelines. Revolving credit gives you a few months of warning through rising utilization and rising minimum payments before things break. Installment credit gives you no warning at all. The payment is the payment. If you miss it, you miss it.

What lenders are actually looking at

When you apply for credit, the lender isn't just checking your score. They're looking at the shape of your file.

- Auto loan applications look at both your installment history (have you handled a vehicle or similar loan before?) and your revolving utilization (are your credit cards maxed right now?). A maxed-out card the day you apply can drop your approval odds even if your overall score is fine.

- Mortgage applications care a lot about credit mix and recent installment behavior. They also look at your debt-to-income ratio — your total monthly debt payments compared to your gross monthly income. A high DTI tanks mortgage approval even with a perfect credit score.

- Credit card limit increase requests care most about how you've used the card you already have. Low utilization, on-time payments, and a few months of activity usually unlock a higher limit.

- Personal loan applications want to see that you can handle a new installment obligation on top of your existing credit cards. If your cards are heavy, the lender assumes the personal loan payment will tip you over.

You're not being judged on a single number. You're being judged on whether the next twelve months of your life look likely to result in on-time payments. The score is a shortcut to that question, not the answer to it.

The traps most people fall into

The cards-only trap. Using only credit cards builds revolving history but leaves your file thin. Your score will climb into the high 600s or low 700s and then stop. The missing ingredient is installment history.

The maxed-card spiral. Paying minimums on cards that are near their limit keeps your utilization sky-high. Your score drops 50–100 points fast, which then makes everything else more expensive — higher interest rates on new cards, higher auto loan rates, sometimes higher insurance and apartment deposits.

The "build credit mix" mistake. Some people, hearing they need both types, will take on an installment loan they can't afford just to add it to their file. This always backfires. A missed installment payment damages your file far worse than a thin file ever would. Don't take on installment debt just for the credit boost — only take it on when the loan is for something you actually need and can actually afford.

The cosigner trap. Cosigning a loan for someone — a partner, a relative, a friend — puts that loan on your credit file as if you took it out yourself. If they miss payments, your score drops. If they default, you owe the balance. The "I'm just helping" framing doesn't change that legally or financially.

Why this matters more when your income varies

If you work hourly with shifting schedules, gig with weekly variance, or freelance with months that come in heavy and months that come in light, the standard credit advice gets sharper.

Variable income makes high utilization more dangerous. A salaried worker with a maxed credit card has a predictable paycheck coming every two weeks to chip the balance down. A gig worker with a maxed card and a slow week has no such guarantee. Keeping utilization low even when you don't need to — 1% to 9% is ideal — gives you headroom for the slow weeks that always come.

Installment payments take a bigger bite of a small month. If your good months bring in $4,500 and your slow months bring in $2,200, a $400 monthly car payment is fine in the good month and brutal in the slow month. The honest math isn't "can I afford this in my best month?" It's "can I afford this in my worst month?"

Income tracking becomes a credit tool. The number that actually matters when you're considering a new loan or a new card isn't your gross income — it's the dollars left over after taxes, expenses, and existing payments. That's the number a loan payment has to fit inside.

A practical playbook

If you're starting from a thin or no-credit file, build slowly and on purpose.

Start by pulling your credit reports for free at annualcreditreport.com — the only official source for free weekly access to your reports from all three bureaus. Look at what's there and what isn't. If you have no credit accounts at all, you have no file yet. If you have only credit cards, your installment side is missing. If you have only an old auto loan and nothing else, your revolving side is missing.

For revolving credit when you're starting out: look at secured cards through credit unions or smaller banks. You put down a deposit, the deposit becomes your limit, and the account reports to all three bureaus like a regular credit card. Use it for one small recurring charge each month — a streaming subscription, your phone bill — and pay it off in full before the statement closes. That's it. The boring use is the powerful use.

For installment credit when you're starting out: credit-builder loans through credit unions are designed for exactly this. You don't actually get the money up front — they hold it, you pay into it, and at the end you get the balance back. Your monthly payments report to the bureaus as a normal installment loan.

Once you have both types of credit on file, the boring rules apply forever: pay everything on time, keep revolving utilization low, don't open too many new accounts in a short period, and don't close your oldest accounts even when you're not using them.

How How Much+ helps you make the actual decision

A credit score gets you in the door. The number that decides whether the loan is a good idea or a bad idea isn't your score — it's your real take-home after everything else is paid.

When you track your income honestly — hourly, gig, passive, all of it — and your expenses honestly, what's left over is your real surplus. Not your gross income. Not your "I think I make about this much." Your actual surplus.

That surplus number is what tells you whether you can afford a new monthly payment. A $250 car payment doesn't fit into $180 of monthly surplus, no matter how much you want it to. A $400 personal loan payment doesn't fit into $300, even with a 780 credit score. The bank will approve you. The math won't.

By the time you're considering new credit, you should already know your average monthly surplus across your last three to six months — including your slow months. That's the ceiling. A new payment that uses more than half of your surplus is risky even when you're approved. A new payment that uses less than a quarter of your surplus is usually safe even when life throws something at you.

How Much+ is built to give you that number. Track for a few months and the surplus becomes obvious. Then when a lender says "you're approved for $X" — you'll know whether $X is actually affordable, or just available.

For the harder questions — should I refinance my auto loan, can I afford this mortgage payment on my variable income, should I consolidate cards, is now a good time to apply — Monty (the chat helper in the bottom-right of How Much+) is built to help you frame the question so the answer is clearer. He can't make the call for you, and he's not a financial advisor, but he can point you toward the right next step.

Take this to a credit counselor or financial professional

Before you act on anything in this article — especially if you're considering a major loan or trying to recover from credit damage — bring these questions to a HUD-approved housing counselor, a nonprofit credit counseling agency, or a licensed financial advisor:

- Based on my actual income pattern over the last 12 months, what monthly payment is realistic for me — not just affordable in my best month?

- Given my current credit file, what's the lowest-risk way to add the type of credit I'm missing?

- If I'm carrying high-utilization credit card debt, should I prioritize paying it down, consolidating it, or negotiating with the issuers — and in what order?

This article was last reviewed on June 5, 2026. It is general educational information, not credit, tax, legal, financial, investment, or accounting advice, and no professional or fiduciary relationship is created by reading it. Credit scoring models, lender criteria, and consumer credit laws change frequently and vary by jurisdiction. Always confirm current rules with an authoritative source and consult a licensed professional for your specific situation before acting.

Have a correction or update? Email legal@howmuchplus.com.

Sources

- myFICO.com — How FICO scores are calculated

- Consumer Financial Protection Bureau — Credit reports and scores

- AnnualCreditReport.com — Free weekly credit reports

Links to third-party sources are provided for reference. How Much+ is not affiliated with these organizations and does not control their content; verify the latest information directly with the source.

You are viewing a static, prerendered version of this page intended for search engines and link previews. The full interactive experience loads automatically when JavaScript is enabled.