Emotional Necessities vs Emotional Goals — The Most Honest Money Conversation You Haven't Had Yet

By How Much+ Editorial Team · Published 2026-06-05 · Last updated: 2026-06-05 · 11 min read

Some emotional spending keeps you operational. Some is a goal in disguise. Learning to tell the difference is the foundation of every budget that actually works — and the start of building money that works for you.

Parts of this article were drafted with AI assistance and reviewed by a human editor. This is general educational content, not personalized advice.

By the How Much+ Editorial Team · Published June 5, 2026

A short note: this article was written with AI as a drafting assistant and edited by a human. It's general information, not personalized advice.

Most personal finance content treats emotional spending like a moral failure. Stop buying coffee. Cancel the subscriptions. Don't eat out. The framing is the same everywhere — your feelings are the problem, and discipline is the solution.

That advice is wrong, and worse, it makes things worse. Here's what nobody tells you: some emotional purchases are keeping you operational. They're the difference between showing up to work tomorrow and not. Take those away and your finances don't improve — they collapse, because you stop being able to earn.

But there's a different category of emotional spending that looks similar on the surface and is actually completely different underneath. That's the spending that doesn't keep you going. It just makes you feel better for a few hours. Then you need more of it. That's not a necessity. That's a goal that hasn't been named yet.

This article is about telling the difference. Once you can see it clearly, your money starts working differently — because you stop fighting with yourself about the spending that's actually serving you, and you start being honest about the spending that isn't. That's the purpose of How Much+: make it clear what's available to change your circumstances.

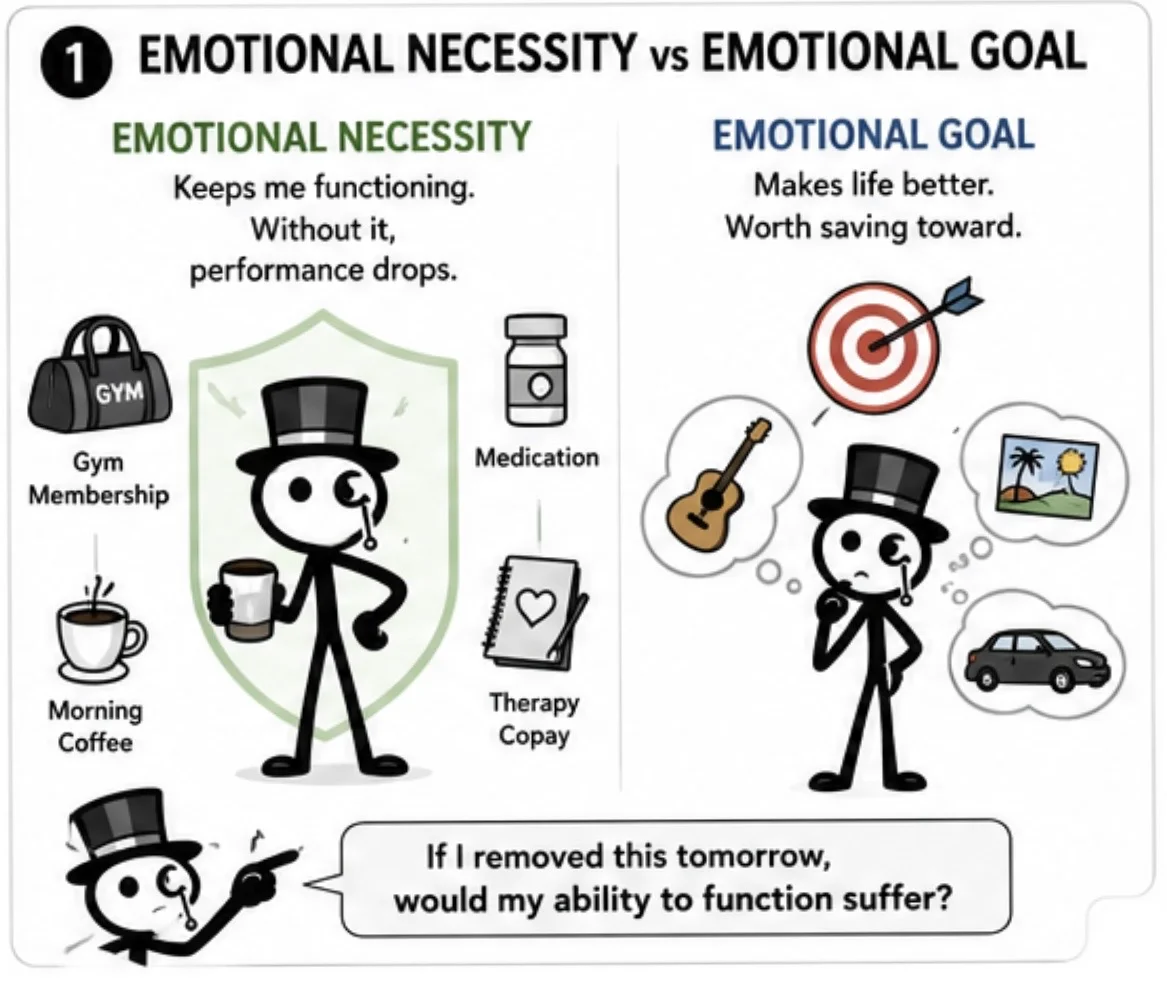

The two categories, defined

An emotional necessity is anything that keeps you operational. It's the absolute bare minimum you need to keep showing up — at work, at home, in your own life. It's not "nice to have." If you remove it, your output drops. Your health drops. Your earning capacity drops.

This is personal. What's a necessity for one person isn't for another. The $4 coffee in the morning might be a luxury for someone who works from home and sleeps eight hours. For someone working a 5 AM shift after putting kids to bed at 11 PM, it might be the one thing that makes the difference between a productive day and a wreck. The coffee isn't the point. The functioning is the point.

An emotional goal is anything you want because it would make you feel better. Not because removing it would break you, but because adding it would lift you. A guitar you've thought about for two years. A trip with someone you love. A weekend somewhere quiet. The car you actually want, not the one that fits the math. These aren't necessities. But they're real, and they're worth funding on purpose.

The trap is treating these two categories as the same thing. The advice "cut out luxuries" lumps them together. Cutting a necessity makes you less functional. Cutting a goal leaves you working hard for nothing in particular. Both feel like deprivation, but only one of them is the kind that builds toward something.

Why the distinction is so personal

Here's where this gets harder. The reason people argue about what counts as a necessity is that the necessities are different for everyone, and most of them are tied to things people don't talk about.

Someone managing chronic pain has different necessities than someone who doesn't. A monthly massage might not be optional — it's the thing that keeps the pain from becoming a missed shift. The acupuncture appointment isn't a treat. It's the difference between working and being laid up.

Someone managing a mental health condition has different necessities than someone who doesn't. The therapy copay is a necessity. The medication is a necessity. The gym membership that's the only thing keeping the depression in check is a necessity. Cancel any of those to save money and you don't actually save anything — you trade $200 a month for two weeks of being non-functional, which costs you more than $200.

For people managing service-connected conditions, chronic pain, PTSD, anxiety, or any of the dozens of invisible things people deal with quietly — the necessities aren't optional. They're the infrastructure that lets you keep earning. Anyone telling you to "just cut back" on the things that keep you operational doesn't understand what you're actually paying for.

The honest version of this conversation is: what is the absolute bare minimum you need to continue forward? Not what you'd like. Not what would be comfortable. The minimum. That's your necessities list, and it should be short and specific to you.

The hard part — being honest about what's actually a goal

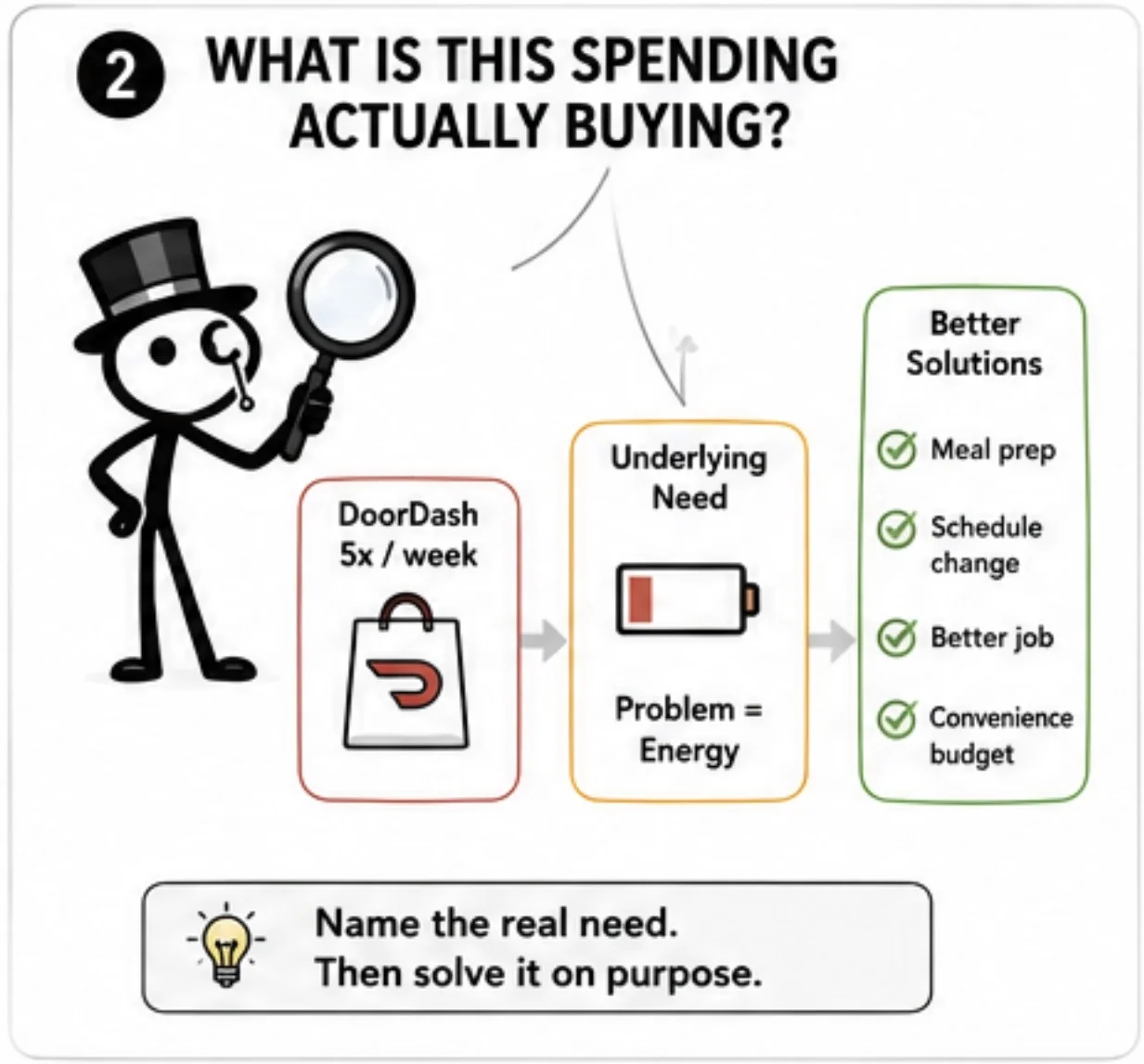

Once you've listed your real necessities, the next step is the one most people skip. You have to look at the rest of the spending and ask: is this keeping me going, or is this just making me feel better right now?

The answer is usually uncomfortable. A lot of what gets called "treating yourself" is actually a goal in disguise — something you'd be happier saving toward intentionally than burning $40 at a time on impulse.

The $80 night out three times a month isn't keeping you operational. It might be standing in for "I want a real social life with people I care about" — which is a goal worth funding deliberately, not an ongoing line item.

The DoorDash habit five nights a week isn't keeping you operational. It might be standing in for "I'm too exhausted at the end of the day to cook" — which is either a goal (find a better job that doesn't wreck you) or a necessity in disguise (your time and energy genuinely don't allow cooking). Only you know which.

The harder cases are the ones that involve the stuff nobody puts in personal finance articles. The substances. The relief habits. The "I just need to get through tonight" purchases. Those don't get named in polite financial advice, but they exist, and they often eat the surplus that would have funded a real goal. The honest accounting includes them, even if the accounting is just for you.

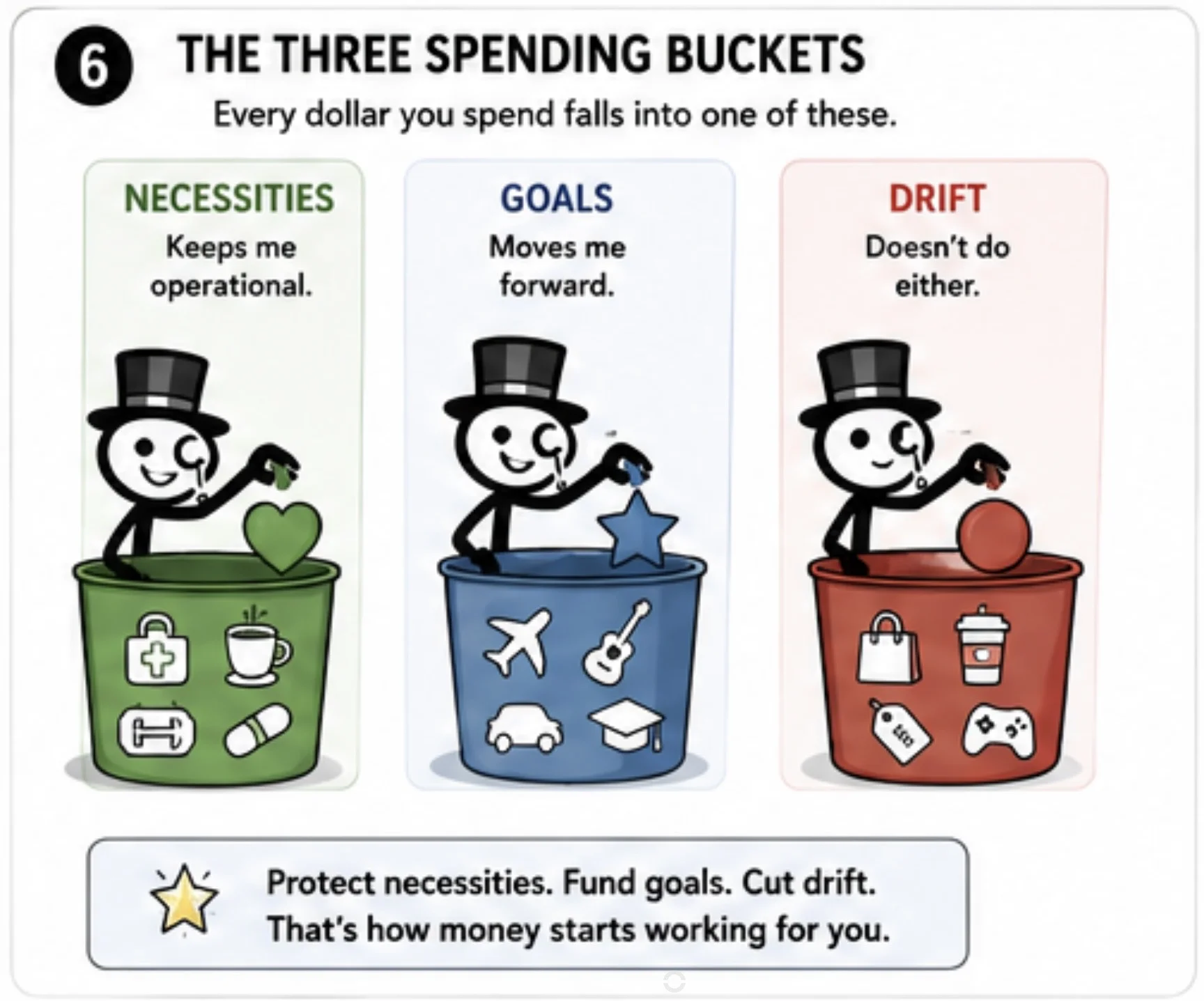

The framework — what to do once you can see the difference

This is where it stops being a values exercise and starts being a money strategy.

Protect your real necessities ruthlessly. Once you've identified what keeps you operational, those line items don't get cut in a budget tightening. Cut anywhere else first. If your necessities are eating too much of your income, the answer is to grow the income, not starve yourself of the things that let you earn.

Fund your goals deliberately. Take the spending you've identified as goals-in-disguise and stop letting it leak out $20 at a time. Pull it together. If you're spending $240 a month on impulse goals, that's $2,880 a year — enough to fund the actual goal hiding underneath. The trip. The guitar. The reliable car. The certification course. Whatever it actually is.

Cut the drift. The spending that isn't operational and isn't building toward anything either — that's the only category that should ever be cut in a tightening. Not your necessities. Not your goals. The drift in between.

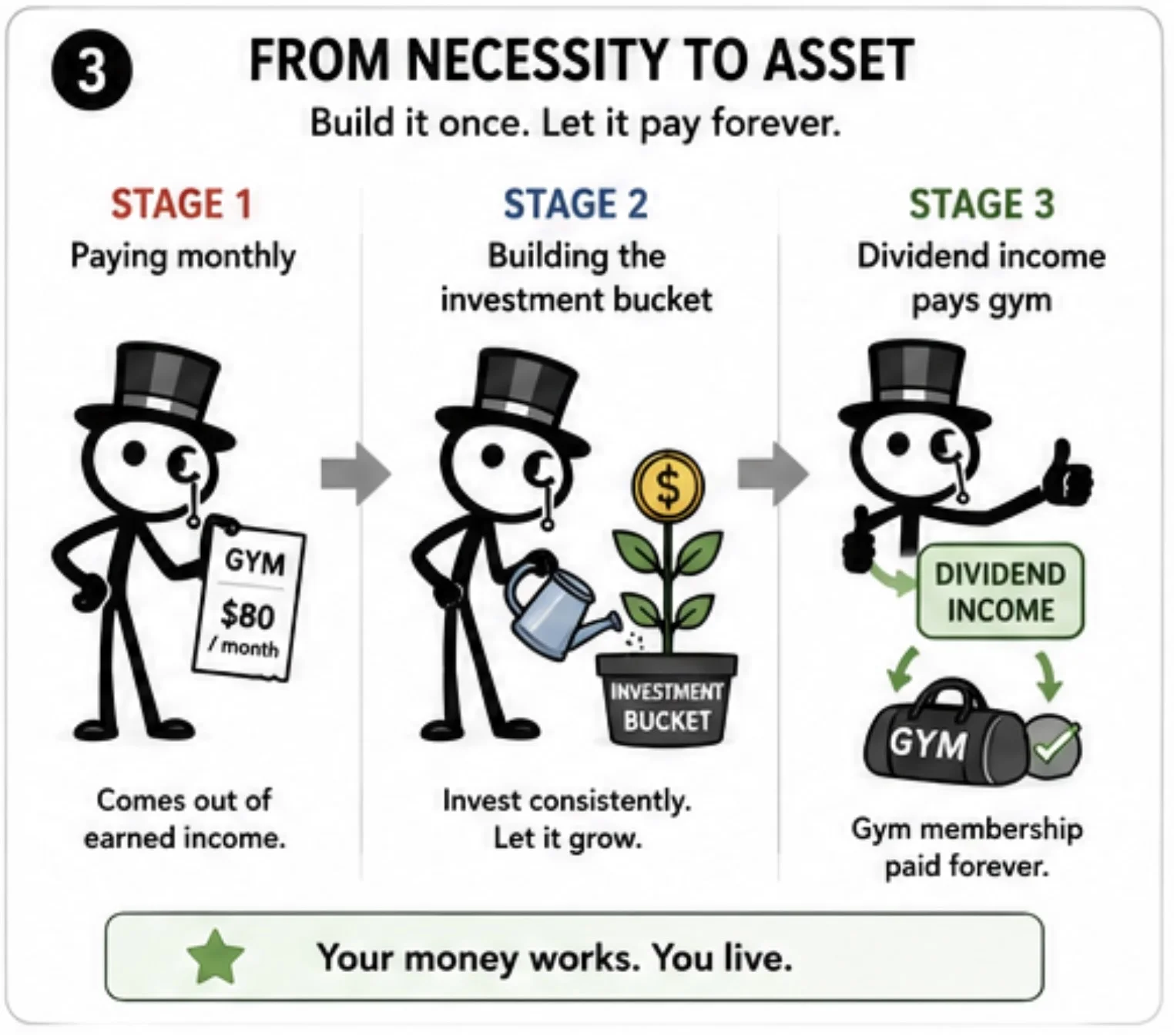

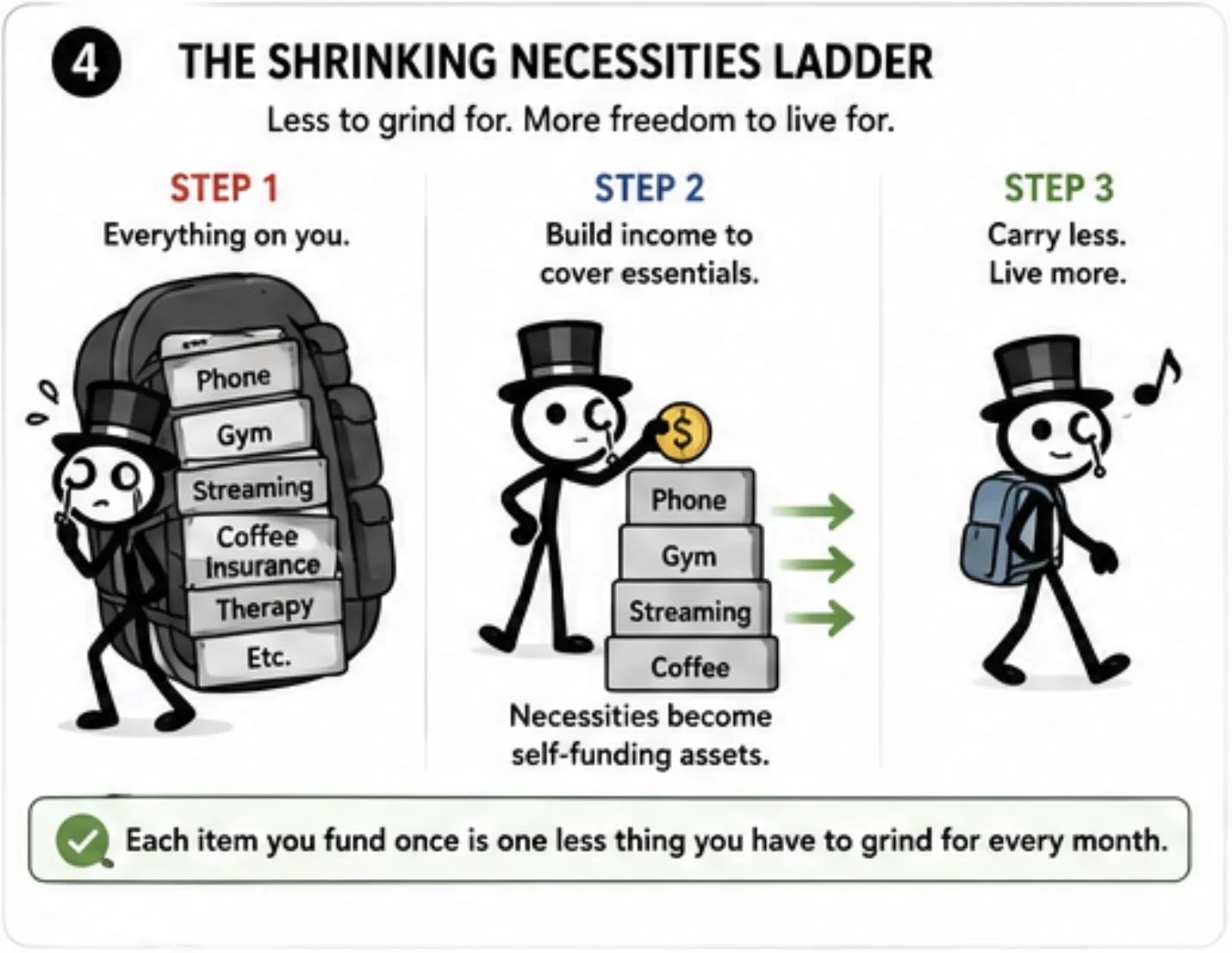

How to make a necessity pay for itself

Take a $80/month gym membership. Most people treat it as a fixed cost forever. Here's another way to think about it.

A dividend portfolio yielding 4% annually needs roughly $24,000 to produce $960/year — your gym for free. That's a lot of money. But if you kick in $100/month while working toward it and reinvest the dividends, you can get there in 10–12 years depending on rates. After that, your gym membership is paid for by your portfolio, for life. The $80/month doesn't come out of your earned income anymore. It comes from money that's working for you.

The numbers are big until you realize you only have to build them once. A $15/month streaming subscription needs roughly $4,500 in a 4% portfolio to pay for itself — reachable in 3–5 years. A $40/month phone plan needs around $12,000. The mechanism is the same: build a small pile of capital that produces enough income to cover a specific recurring expense, then enjoy that expense forever as a free luxury.

There are also smaller, faster moves: annual gym payment instead of monthly often saves 15–20%. Generic medication versions, where appropriate, can cut prescription costs by 80%+. The point is to stop treating necessities as fixed costs you have to grind for forever. Each one is a target. Each target can be reduced, shifted, or eliminated as a real expense from your earned income.

When a necessity transitions into a goal

Once a necessity is paying for itself — through a small portfolio, through a clever income arrangement, through whatever method works — something interesting happens to your relationship with it. It stops being a thing you have to maintain. It becomes a thing that's just there. The pressure is gone.

At that point it's no longer a necessity in the operational sense. You don't need it to keep going anymore, because you've built the machinery that maintains it. It's an asset you've earned, not an obligation you're managing.

This is the transition the article framing exists to make visible. The list of things that keep you operational today isn't supposed to be your list forever. Each item on it is a candidate for the same treatment — identify the real cost, build the income to cover it, free up the earned income for the next thing.

After enough cycles of this, the list of things you have to grind for shrinks, and the list of things you can pursue purely as goals grows. That's what financial freedom actually looks like in practice. Not "never spending money on yourself." The opposite. Spending money on yourself easily, because the spending is funded by the money you've built instead of the money you have to earn fresh every month.

The gut-check question for big decisions

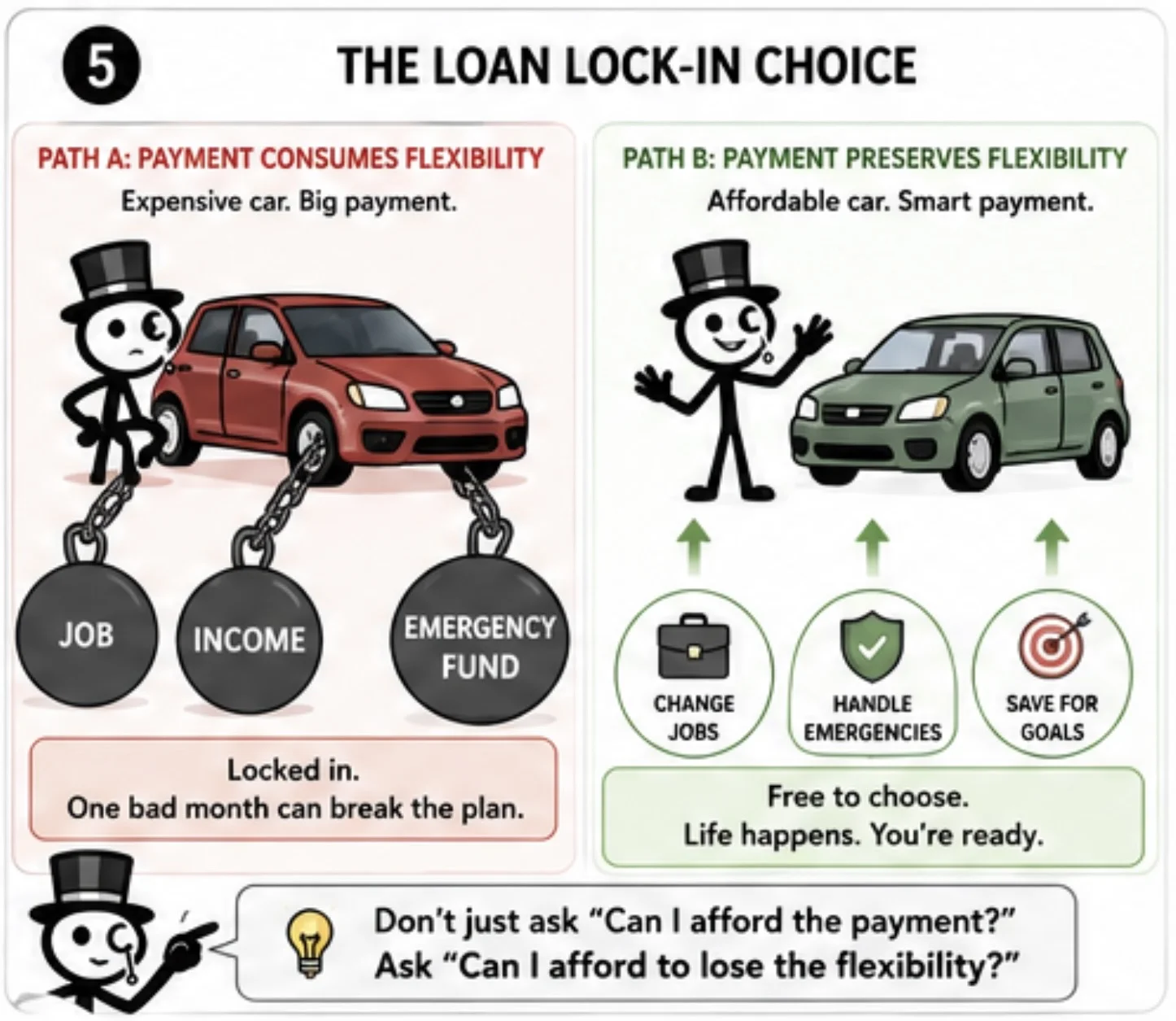

The framework changes how you think about large purchases too. Especially the ones that lock you in for years.

Take a car loan. The standard advice is to look at the payment as a percentage of monthly income — if it's under 15%, it's "affordable." That's incomplete advice for anyone with variable income, anyone with health considerations, anyone whose life might shift in the next 5 years.

The better question: would a loan that takes 50% of your paycheck be worth it if you have to stay at your job for the next 5 or 6 years and can't have any unexpected expense ruin your plan? When you frame it that way, the answer is almost always no. The car wasn't the problem. The lock-in was. The vulnerability to one bad month was. The fact that the loan would consume not just your money but your flexibility — that was.

The same question applies to a mortgage, a personal loan, a payment plan on furniture, a financed phone. Not "can I afford the payment?" but "can I afford to lose the flexibility?"

How Much+ is built to help you see the answer to that question clearly. When you track your real income and your real expenses honestly, your monthly surplus becomes a number you can trust. Not your gross. Not your best month. Your actual leftover, including the slow months. A new payment that uses more than half of that number is dangerous regardless of credit score or lender approval. A payment that uses less than a quarter of it is usually safe even when life surprises you.

The bottom line

Stop fighting yourself about money. The things that keep you operational aren't moral failures — they're infrastructure. Fund them honestly, and where you can, build the smaller machine that pays for them so you don't have to.

The things that are pulling you forward — the real goals — deserve their own line. Name them. Fund them on purpose. Don't let them leak out in impulse purchases that don't actually deliver the thing you wanted underneath.

And the things in between — the spending that isn't operational and isn't building toward anything either — those are the only things that should ever get cut in a tightening. Not your necessities. Not your goals. The drift in between.

For the harder questions — what's actually a necessity in your specific situation, how to start a dividend portfolio, when a payment plan crosses from manageable to dangerous — Monty, the helper in the bottom-right of the How Much+ app, is built to point you to the right next step. He can't make the call for you and he's not a financial advisor, but he can help you frame the question so the answer becomes clearer.

The accounting is honest, or it doesn't work. Start there.

Sources

- Consumer Financial Protection Bureau — Budget planning and debt-to-income guidance

- Investor.gov (SEC) — Compound interest and dividend investing basics

- National Alliance on Mental Illness (NAMI)

- SAMHSA National Helpline — 1-800-662-4357

Links to third-party sources are provided for reference. How Much+ is not affiliated with these organizations and does not control their content; verify the latest information directly with the source.

You are viewing a static, prerendered version of this page intended for search engines and link previews. The full interactive experience loads automatically when JavaScript is enabled.